Where Retirement Clients Go To Become Friends and Private Clients

Create A Safe and Secure Retirement Plan

Our Mission is to protect American families' wealth and create a retirement income that can last their lives.

A Personalized Private Client Relationship

Protecting wealth so you can focus on what matters most to you.

01. About Us

We are dedicated to providing safe and secure strategic retirement planning that is right for you. Simply put, we strive to be our client’s trusted wealth advisor. We are a low-risk, low-fee retirement planning firm that serves families seeking a safe, secure, and tax-efficient retirement plan.

02. Our Process

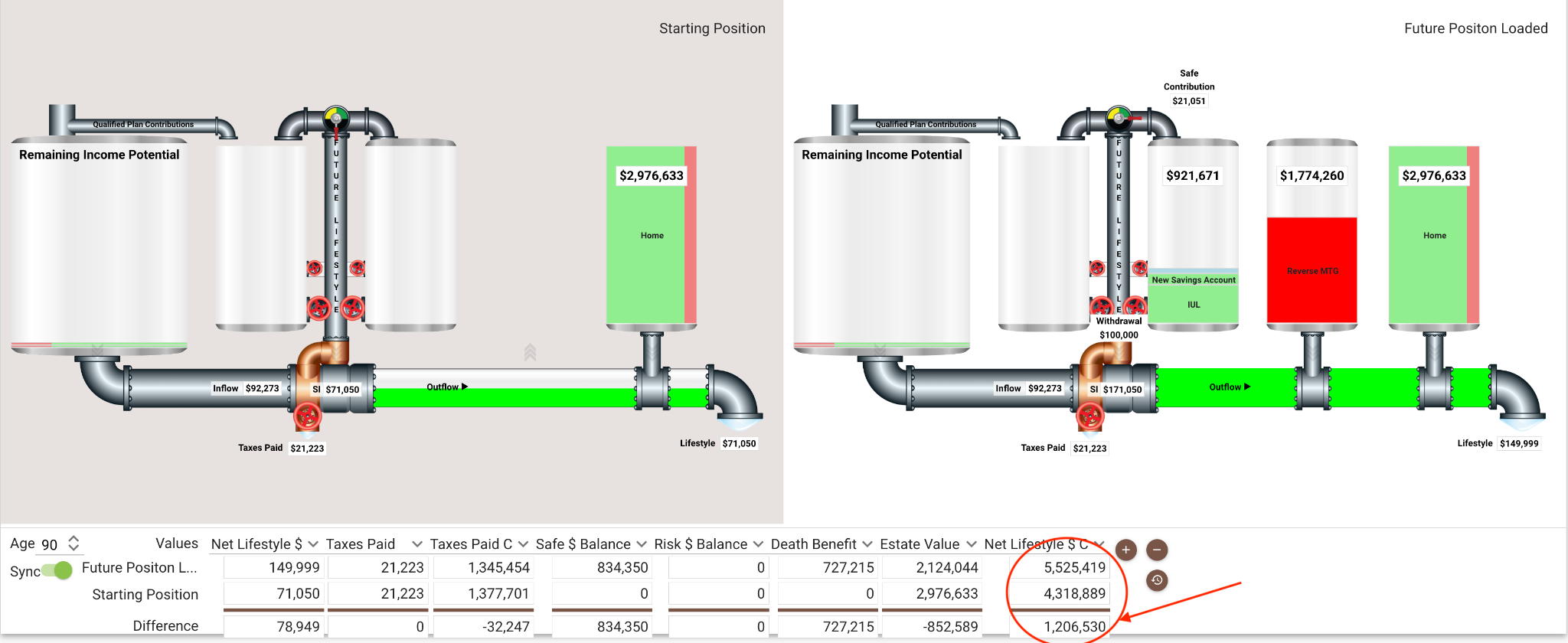

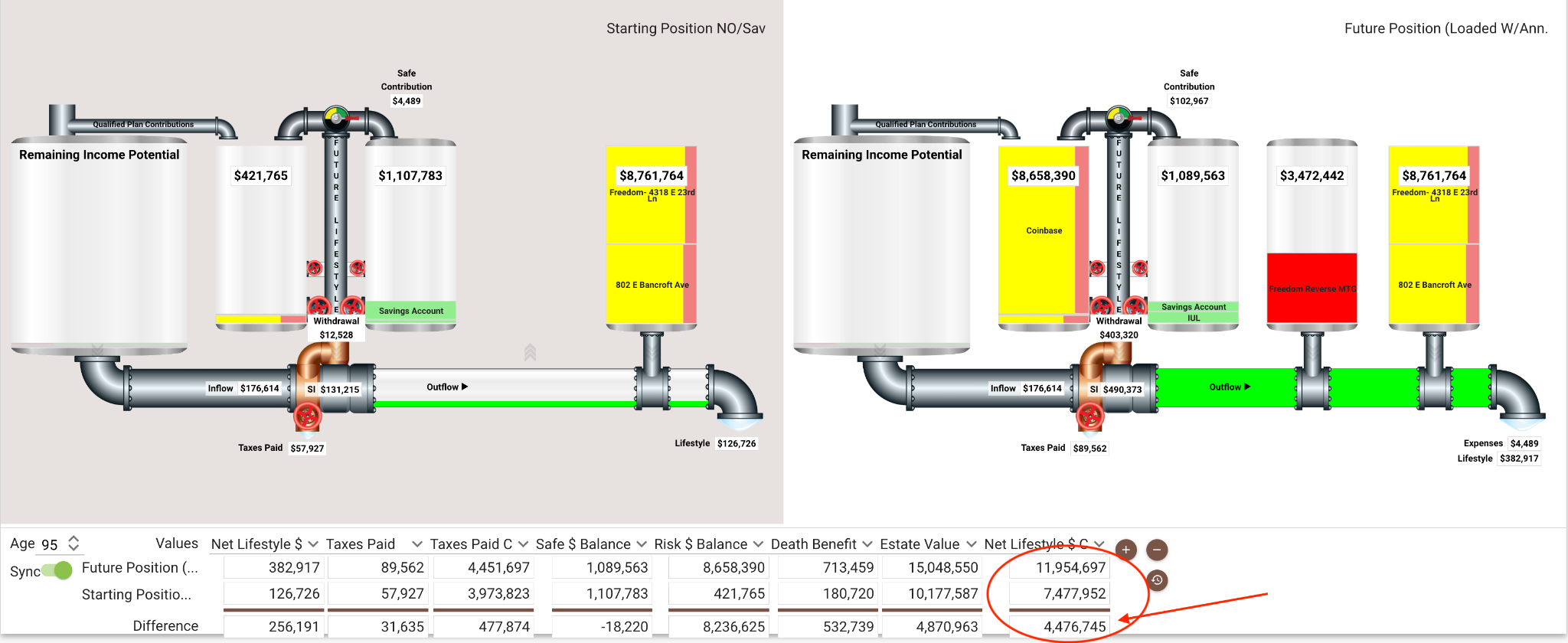

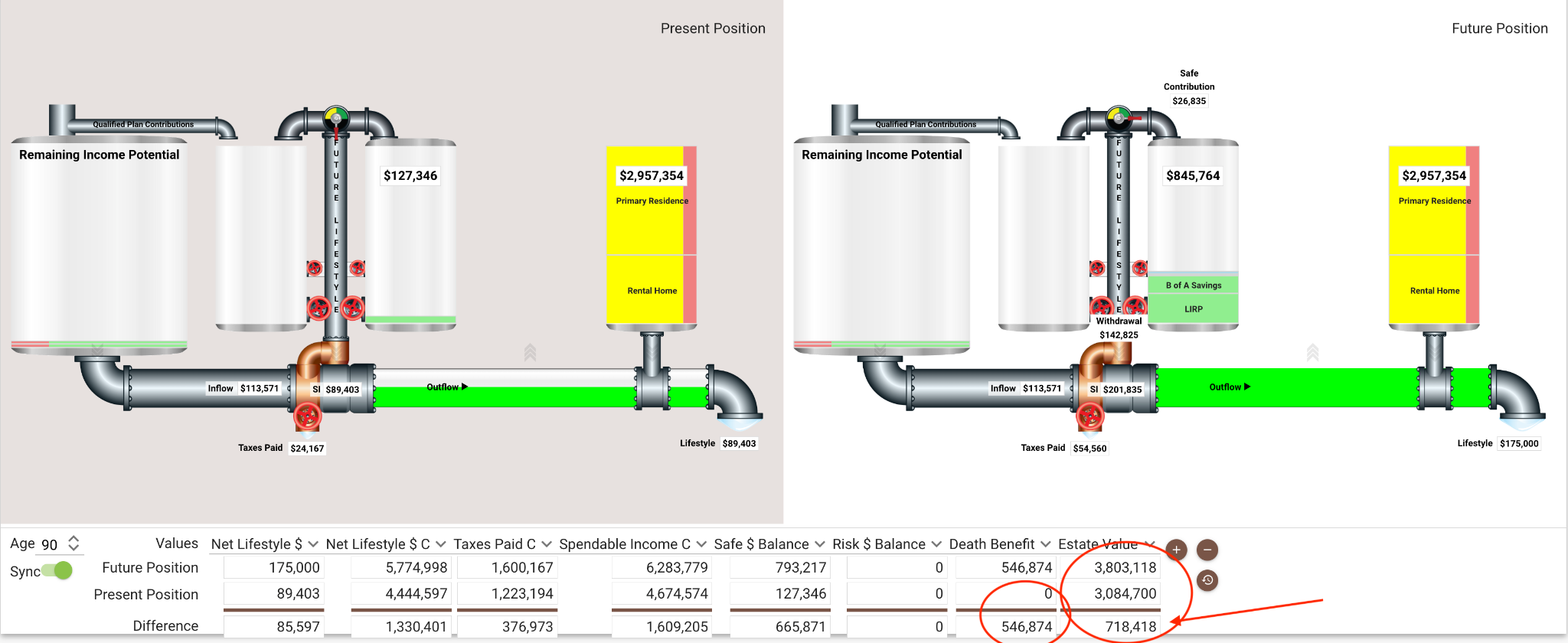

Discover the Private Client Group's innovative Three Phases Wealth Protection and Retirement Income Blueprint, designed to safeguard your wealth from market losses and enhance your retirement and estate plan by at least $1,000,000. Unlike traditional approaches, this personalized blueprint, created within 30 days, focuses on preserving your wealth, minimizing retirement income taxes, and providing a guaranteed lifetime income without sacrificing your current lifestyle. Simply follow the steps in the correct order, and we'll be with you every step of the way.

03. Our Philosophy

We are a retirement planning firm that creates a personalized economic model to help you achieve your financial goals. We'll present your model, current position, and future position in a meeting.

Our Services

Retirement planning today has taken on many new dimensions that never had to be considered by earlier generations. For one, people live longer, and inflation and rising income taxes constitute a significant problem. A person who turns sixty-five today could be expected to live as many as thirty-five years in retirement compared to a retiree in 1950 who lived, on average, an…

Insurance is essential to any comprehensive financial security plan. If tragic events like death, disability, or critical illness strike, insurance can protect you and your family from undue hardship. Some life insurance policies also provide tax-advantaged savings that you can draw on to achieve...

Want to know the secret of financial well-being? It’s not as much about what you do to accumulate more but how effectively you can utilize it. Efficiency is the name of the game. The key lies in discovering how to balance your current lifestyle desires with your future lifestyle requirements.

“THERE ARE ONLY TWO WAYS TO IMPROVE YOUR PRESENT FINANCIAL POSITION. ONE IS TO FIND BETTER PRODUCTS, WHICH MAY POTENTIALLY PAY HIGHER RATES OF RETURN BUT WHICH OFTEN REQUIRE MORE RISK. THE SECOND IS TO BE MORE EFFICIENT BY AVOIDING UNNECESSARY LOSSES ALONG THE WAY.

THERE IS MORE TO BE GAINED BY AVOIDING THE LOSSES THAN TRYING TO PICK THE WINNERS.”

Our Mission

Our Mission is to protect American families' wealth and create a retirement income to last their lives.

We will serve our clients at the highest level and strive to ensure that every client feels like a private client.

Your future is calling, and we're here to answer. Let's start building the retirement you've always dreamed of. “There’s a big difference between wealth and income.

Knowing I have a million dollars doesn’t tell me the lifestyle I can enjoy from that million. What we care about is the lifestyle.

So you can forget fund values; income is all that matters. Knowing how much money you have doesn’t tell you how to live. You need to know how much you can buy.

The primary concern of the saver remains what it always has been: Will I have sufficient income in retirement to live comfortably?”

The Private Client Company will answer these questions for you.

The Retirement Deception was filmed to expose the truth about a successful retirement. The Private Client Company is a proud executive producer of the film.

The producers traveled over eighteen thousand miles and interviewed dozens of actual retirees and financial experts about the myths and misconceptions Wall Street has perpetrated on the public about how to retire happily. What they discovered is surprising, although not shocking, if you understand Wall Street's motivation. A successful retirement is about something other than a significant nest egg, a high rate of return, or hoping that the market goes up. Watch this film to see real-world Americans who have retired successfully and how they did it.

If you would like to watch the film, please message us the on the right-hand side of this website in the chat, and we will provide you with a complimentary access code to your email.

Testimonials

“I have worked with Jim and his team several times. They are thorough, extremely knowledgeable, and have helped me see my future financial position clearly and with equanimity.!” Thank you.

-AJ- ID

“Everyone is friendly and helpful, prompt and great communication. Never felt like we were less important than someone they were working with simultaneously.” I recovered 2.M of the money I was transferring away unknowingly and unnecessarily to the tax man and my mortgage company..

-Jessica- WA

"Jim and the team are my trusted financial strategists, not only to us but to our family and many friends. We ALWAYS refer them when the topic of retirement planning comes up."

-JoAnn-CA

Working with Jim has been a lifesaver for us. Going through the Wealth Protection Blueprint process with him was genuinely eye-opening, to say the least.

We thought we were ok, and we did. We had saved almost a million dollars in our 401k, and our home was nearly paid off. We were utterly blown away when we learned that we would run out of money during our retirement years at age 77. Once Jim worked with us to build our new financial position for the future, we saw how our retirement would be attainable and completely secure, and we were elated. He made the one million dollar difference he said he would help us find in the end as well.

We will refer everyone to The Private Client Company for their retirement strategies. Thank you

RC Hayes - 11/23

When I first met with Jim over Zoom, I knew I hadn’t saved enough money for retirement. I also knew the stock market and future income taxes would eat my lunch.

As a busy MD, I need more time to study the markets, etc.

Truthfully, I didn’t want to see the reality of my situation.

That’s when Jim went to work with me and (for) me to build the retirement strategy I can understand. As a result, I am not only on track for my retirement, I plan on retiring eight years earlier than my original retirement goal, and I have an extra four point four million dollars added to my estate.

I can't thank Jim enough for the time, knowledge, and energy he put into my retirement strategy. I am forever grateful.

Dr. Andrews - 4/22

I am writing this testimonial with sincere gratitude for Jim Stryker and the rest of The Private Client Group; I am the first to admit it. I am a challenging client for anyone. I am a numbers gal, digging deep and asking many questions!

Jim is a financial professional like no other for me; he never rushed the process, and he never tried to sell me anything.

Jim took his time and helped me understand what I needed to know about my current financial plan and that I was headed down the wrong path.

Thank you, Jim, for taking me on and everything you have done to assist me.

S Marks - 8/21

FAQ’s

Here are some frequently asked questions (FAQs) about retirement planning strategies along with their answers:

Q: Why is retirement planning important?

A: Retirement planning is crucial to ensure financial security during your non-working years. It helps you maintain your desired lifestyle and covers essential expenses when you no longer have a regular income.

Q: When should I start planning for retirement?

A: It's never too early to start. Start in your 20s or 30s to take advantage of compounding interest and have a longer investment horizon. However, there is always time to begin planning.

Q: What are the key components of a retirement plan?

A: A comprehensive retirement plan includes setting goals, estimating retirement expenses, determining income sources (e.g., pensions, Social Security, investments), and creating a savings and investment and de-accumulation strategy.

Q: What role does Social Security play in retirement planning?

A: Social Security can be a significant income source in retirement. Understanding how it works, when to start benefits, and how it fits into your overall retirement income strategy is important.

Q: What is the 4% rule in retirement planning?

A: The 4% rule suggests that withdrawing 4% of your retirement savings annually should provide a sustainable income for at least 30 years. However, this rule is a guideline, and adjustments will be needed based on market conditions and individual circumstances.The 4.0% rule is now the 2.4% rule!

Q: How do healthcare costs factor into retirement planning?

A: Healthcare costs tend to rise in retirement. Factor in expenses like insurance premiums, out-of-pocket costs, and long-term care.

Q: Should I seek professional advice for retirement planning?

A: Consulting with a wealth protection and retirement income specialist can provide personalized guidance based on your goals and financial situation. They can help optimize your retirement plan, manage risks, and adapt strategies as circumstances change.

Remember, individual circumstances vary, and consulting with a financial professional for personalized advice tailored to your situation is advisable.

Disclaimer

Retirement Planners at The Private Client Company do not provide specific tax/legal advice, and this information should not be considered as such. You should always consult your tax/legal advisor regarding your particular tax/legal situation.

Separate from the financial plan and our role as a financial planner, we may recommend purchasing specific insurance products or accounts. These product recommendations are not part of the retirement plan, and you are not obligated to buy any product.

Life insurance products contain fees, such as mortality and expense charges (which may increase over time), and may contain restrictions, such as surrender periods.

We Help you fortify your nest egg against the 6 biggest risks

Protection risk

An untimely death or accident can create additional stress and financial pressure on our closest loved ones if we don´t plan ahead.

Market Risk

A single 20% or 30% market crash can not only hurt your account balances, but ir can cause you to run out of money years sooner.

Tax risk

CPA and Tax Expert Ed Slott says "Taxes are a larger risk than marker crashes." If you have all your retirement income in qualified plans like IRA´s and 401(k)´s that require you to pay taxes when you take the money out, you have a huge tax leability.

Health care risk

Statics show that long trem health care cost can be the largest expense in retirement what have you done yo protect your nest egg and your family from being hammered by this expense?

Income depletion risk

Will your nest egg provide enough income to give you the retirement you want, for as long as you live? Most people have no idea.

Longevity risk

Longevity is the great RISK MILTIPLIER. Do you know how long you will live? Hopefully a long posperous life. Longer life spans multiply the likelihood of each of these risks happening to you.

If you don’t have a plan in place RIGHT NOW to protect against these six retirement risks, then

request a consultation with The Private Client Company today.

You’ll see how to survive and thrive in retirement while protecting yourself against each of

these six harmful retirement risks.

Office *By appointment ONly!

418 E Lakeside Ave, Coeur D'Alene, ID 83814

All content on this website is for informational purposes only and is not intended as investment advice or as a recommendation to buy, sell, or reallocate any security. I am not a registered investment advisor and do not provide advice regarding securities, managed accounts, or portfolio allocation. All insurance products discussed are non-securities and are offered through life insurance license only.

Copyright © 2025. The Private Client Company, LLC